Pass-throughs account for more than half of the businesses in America, and for the vast majority of small businesses. The tax reform law allows these business owners, if earning less than $157,500 ($315,000 if filing jointly), to take the new deduction. It excludes some companies whose owners earn more than that from taking the deduction because they are a certain type of service business, such as a physician’s or attorney’s office. It limits the deduction for other businesses based on how much they spend employing workers. Many of our business clients were left wondering if they qualified.

The IRS has finally gotten around to issuing some guidance mid-August on how the Section 199A Deduction should be applied, but the exceptions and eligibility rules will not please everyone.

After December 31, 2017 and before January 1, 2026, the deduction allowed is equal to 20% of the taxpayer’s “qualified business income” earned in a “qualified trade or business.” The deduction is generally equal to the lesser of 20% of the qualified business income (QBI), plus 20% of qualified real estate investment trust (REIT) dividends and qualified publicly traded partnership income; OR 20% of taxable income minus net capital gains.

The definitions of “qualified business income” and “qualified trade or business” are important. So are the “income limits.”

Income Limits:

- The deduction is available to taxpayers whose taxable incomes fall below $315,000 for joint returns and $157,500 for other taxpayers

- If you are above the threshold amounts, you are subject to limitations and exceptions which are determined by your service trade or business, and a wage and capital limit.

Qualified Business Income is defined as the net amount of qualified items of income, gain, deduction and loss with respect to a qualified trade or business within the United States only. Employee wages, capital gain, interest and dividend income are excluded. QBI must be calculated for each separate qualified trade or business. If you have multiple businesses, you calculate QBI for each and net the amounts. If you have a negative QBI after you net the amounts, you can carry that amount forward to the next tax year: “If the net amount of qualified business income from all qualified trades or businesses during the taxable year is a loss, it is carried forward as a loss from a qualified trade or business in the next taxable year.”

The deduction is limited for taxpayers with income in excess of the aforementioned threshold, however, to the greater of:

- 50% of the W-2 wages with respect to the qualified trade or business, or

- The sum of 25% of the W-2 wages with respect to the qualified trade or business, plus 2.5% of the unadjusted basis immediately after acquisition of all qualified property.

The resulting deduction is then subject to a second limitation equal to 20% of the excess of:

- The taxable income for the year, over

- The sum of net capital gain as defined

QBI Exclusions Include:

- Any item of short-term capital gain, short-term capital loss, long-term capital gain, or long-term capital loss;

- Dividend income, income equivalent to a dividend, or payment in lieu of a dividend described in Section 954(c)(1)(G);

- Any interest income other than interest income properly allocable to a trade or business;

- Net gain from foreign currency transactions and commodities transactions;

- Income from notional principal contracts (NPC);

- Any amount received from an annuity which is not received in connection with the trade or business, and

- Any deduction or loss properly allocable to the items described in the bullets above;

- Reasonable compensation paid to the taxpayer by any qualified trade or business of the taxpayer for services rendered with respect to the trade or business,

- Any guaranteed payments described in Section 707(c) paid to a partner for services rendered with respect to the trade or business, and

- Any payment described in Section 707(a) to a partner for services rendered with respect to the trade or business.

Qualified Trade or Business – A qualified trade or business is any trade or business, with two exceptions:

1. Specified service trade or business (SSTB), which includes a trade or business involving the performance of services in the fields of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, investing and investment management, trading, dealing in certain assets like stocks, securities or commodities, or any trade or business where the principal asset is the reputation or skill of one or more of its employees. This exception only applies if a taxpayer’s taxable income exceeds the $157,500/$315,000 aforementioned thresholds. Because the two W-2-based limitations also do not apply when taxable income is below these thresholds, a taxpayer in a SSTB with taxable income below the thresholds simply deducts 20% of any qualified business income (subject to the overall limitation).

Based on the explanation of a SSTB, we can assume this applies to the following:

- Doctors, pharmacists, nurses, dentists, veterinarians, physical therapists, psychologists, and other similar healthcare professionals who provide services directly to a patient.

- Lawyers, paralegals, legal arbitrators, and mediators.

- Accountants, enrolled agents, return preparers, financial auditors, bookkeepers.

- Actors, singers, musicians, entertainers, directors.

- Athletes, coaches, team managers.

- Financial advisors, investment bankers, wealth planners and retirement advisors who provide financial services to clients including M&A advisory, and valuation work.

- Engineering and architecture were specifically removed from the list

Real estate brokers, property managers, architects, engineers, and bankers will get the deduction regardless of income level, because they are not engaged in a SSTB. Ditto, if your reputation makes you millions, as long as not any of those $$$ come from endorsements, likeness rights, or appearance fees. Regardless of how integral your reputation is to your business, that business will not be treated as a SSTB, unless it is engaged in one of the specifically delineated disqualified fields.

2. Performing services as an employee not an owner in a qualified business.

To put it more simply –

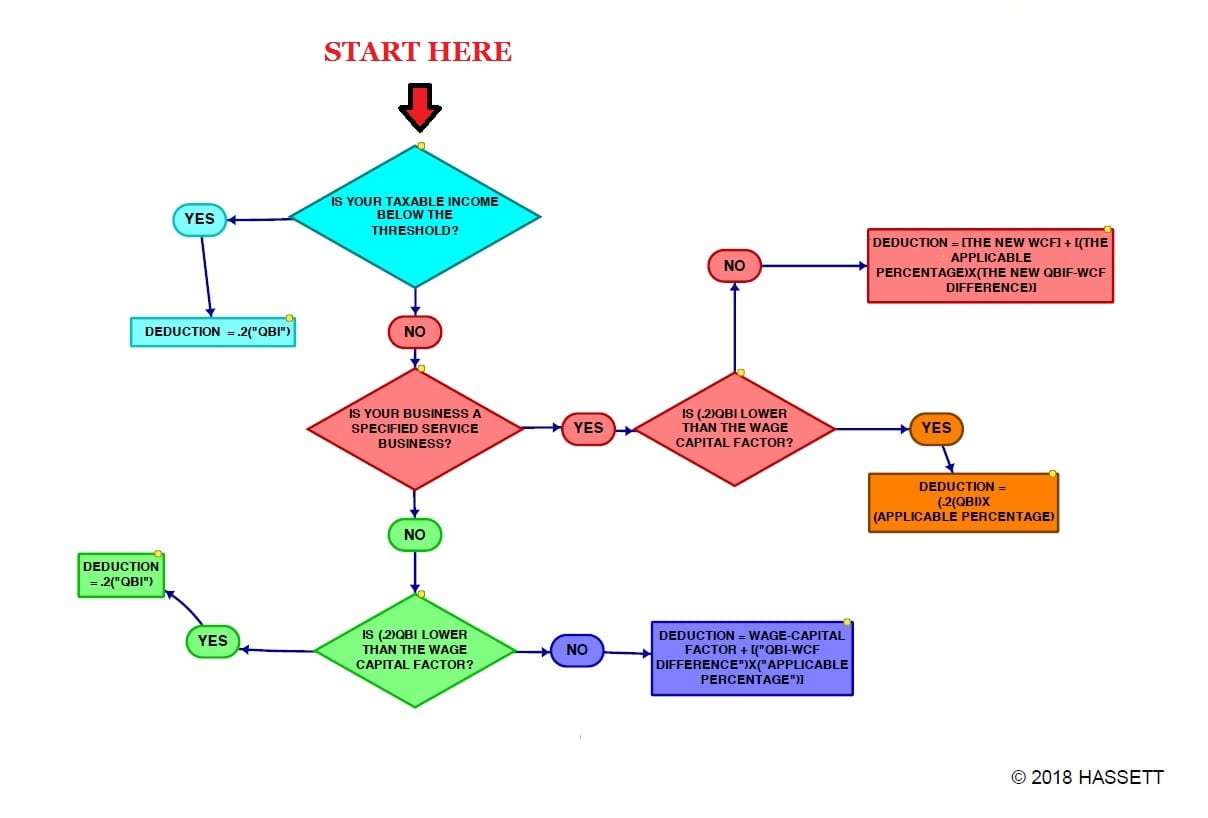

If you own a pass-through business entity and are below the threshold amount, this is the easy way to figure your deduction: The deductible amount for each of your businesses is simply 20% of your QBI with respect to each business. For example, if your income is $50,000 and your QBI is $40,000, then your deduction is $8,000, or 20% of your QBI. You’re under the threshold amount so no need to jump through any more hoops.

If you own a pass-through business entity and are over the threshold amount, this is the how to figure your deduction which may be limited based on:

- If your business is an SSTB as defined above;

- The W-2 wages paid by the business; and

- Unadjusted basis immediately after acquisition (UBIA) of certain property used by the business.

Wage and capital limitation “phase in:”

Taxpayers between the taxable income thresholds and who are not in a SSTB are subject to only a partial wage and capital limitation. The deductible QBI amount for a business of a taxpayer with taxable income between the thresholds is 20% of QBI, less an amount equal to a “reduction ratio” multiplied by an “excess amount.”

The “reduction ratio” is calculated as the amount of taxable income in excess of the lower threshold amount of $315,000 for married filing jointly ($157,500 for other taxpayers), divided by $100,000 for joint filers ($50,000 for other taxpayers). The more taxable income, the higher the reduction ratio, and the more the wage and capital limitations apply until they are fully phased in at $415,000 (or $207,500).

The “excess amount” is the difference between (1) the deductible QBI amount of the qualified business with no wage and capital limitation (i.e., 20% of QBI); and (2) the deductible QBI amount of the qualified business with a fully phased-in wage and capital limitation. The reduction ratio is applied to this amount to determine the reduction of the wage and capital limitation.

Additional Considerations for Clients:

Were you a taxpayer that got a bit impatient after Section 199A came out, and jumped onto the “cracking” opportunity, spending time and money to establish a new rental or administrative entity that just became a disqualified SSTB? BEWARE! Companies will not be allowed to restructure to game the rules. It outlaws a strategy known as “crack and pack,” where business owners split their operations into separate entities like one that owns the doctor’s office and another that provides the medical care to avoid prohibitions on taking the deduction.

By virtue of two pieces of Section 199A – the inclusion of wages paid to an owner in the W-2 limitation and the exclusion from QBI of reasonable compensation and guaranteed payments paid to an owner – inequities arise at all income levels. You might be a sole proprietor with income above the taxable income threshold that’s taking a hard look at converting to an S-corporation, paying a small salary, and maximizing the Section 199A deduction.

In order to determine how best to structure a business for tax purposes, it will be necessary to take into account many factors. Owners of S-Corporations may be able to avoid a substantial amount of Social Security and Medicare/Self-Employment taxes which can add income. Actions that lower your self-employment tax may decrease your pass-through deduction. Also, with the additional change of the corporate rate to a flat rate of 21%, it is not possible to determine whether taxation as a proprietorship, partnership, S- Corporation or C-Corporation will be optimal without knowledge of each business’ unique circumstance and financials.

In light of the newly released guidance, please note there are special considerations in these certain areas:

- Rules for landlords and owners of rental property.

- Some special UBIA rules apply, including a reduction in basis for non-business use of property, and a restriction on property acquired and disposed of near the end of the taxable year without having been used in a trade or business for at least 45 days.

- A de minimis exception that will allow a business that both sells product and performs services to avoid being treated as a SSTB.

- Like-kind exchanges, 1231 losses, and special rules for Aggregation of Commonly Controlled Businesses.

- Three methods to compute W-2 wages for the purposes of the deduction.

- IRS may issue regulations to prevent taxpayers from establishing multiple non-grantor trusts or contributing additional capital to multiple existing non-grantor trusts in order to avoid federal income tax.

- Treatment of a fiscal year business with a year straddling January 1, 2018.